I raised capital when I wasn't ready for it. I scaled before systems existed to support it. Some of those decisions worked, briefly. Others created problems that didn't surface until much later, when fixing them was far more expensive than preventing them would have been. After 12 exits and a five-year research project, I can tell you this: capital is not neutral. It changes behavior, incentives, and power structures the moment it enters a company.

Knowing how to get startup funding means understanding that the fundraising process changes at every stage. What works for a pre-seed raise won't work for a Series A because the investors, expectations, and required materials all change.

This guide maps the entire funding journey from the first dollar to growth-stage capital, with clear guidance on what each stage requires and how to prepare.

The Funding Stages

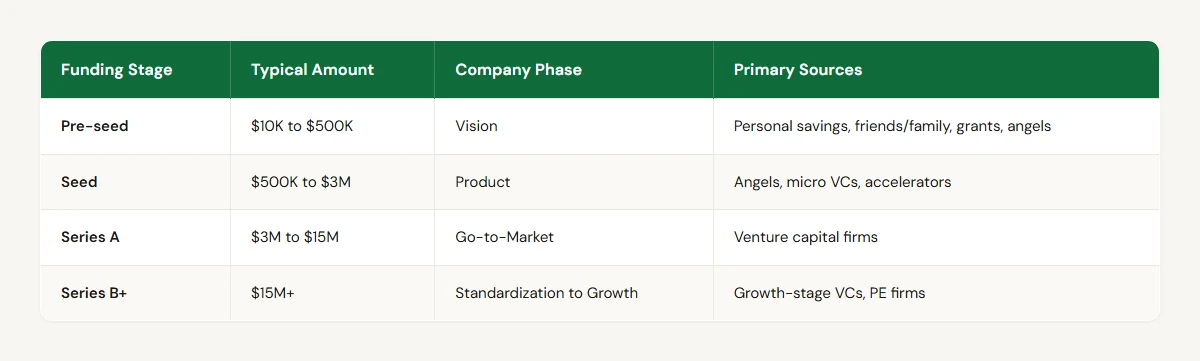

Startup funding follows a sequence that maps to the startup lifecycle. Each round corresponds to a phase of company development:

According to Carta, pre-seed rounds skew small, with deals under $250K making up 44% of all pre-priced rounds in Q4 2024.1 For seed and Series A, Carta reported a median seed round of roughly $2.5M and a median Series A round near $12M in 2024.2

This guide focuses on Pre-seed through Series A, which is where the majority of founders are actively fundraising.

Pre-Seed: The First Capital

Pre-seed funding gets you from idea to prototype. The capital comes from sources that bet on people, not products.

Personal savings and bootstrapping. Most startups begin with founder capital. The dollar amount matters less than what it signals: you believe in this enough to put your own money in first.

Friends and family. Keep these investments structured. Use a SAFE (Simple Agreement for Future Equity) or convertible note. Informal handshake deals cause problems when professional investors show up later.

Grants. Non-dilutive capital with no repayment requirement. Federal programs (SBIR, STTR), state economic development grants, and private foundation grants are all available at this stage. For nonprofits, the landscape is even broader, as covered in our guide to startup grants for nonprofits.

Microloans and CDFIs. For founders who need small amounts ($5K to $50K) and have reasonable personal credit. Our guide on startup business loans with no revenue covers these options in detail.

Angel investors. Individual investors who write checks from $5K to $250K. Angels evaluate the founder, the market, and the problem more than the product. At pre-seed, the product may not exist yet.

What investors expect at pre-seed: A compelling problem statement, a founding team with relevant experience or deep conviction, and early evidence of demand (customer conversations, waitlist signups, LOIs).

Seed: Building the Product

Seed funding gets you from prototype to product-market fit. The capital supports development, early hiring, and initial customer acquisition.

Micro VCs and seed funds. Firms like Precursor Ventures, Hustle Fund, and Uncork Capital specialize in seed-stage investments. Check sizes typically range from $250K to $1M.

Angel syndicates. Groups of angels who pool capital through platforms like AngelList. Syndicate leads curate deals and individual angels participate.

Accelerators. Programs like Y Combinator, Techstars, and MassChallenge provide seed capital alongside mentorship and network access. Our list of the best startup accelerators covers the top programs and their terms.

What investors expect at seed: A working product (or advanced prototype), initial user feedback, a clear business model hypothesis, and a founding team that can execute. A strong pitch deck is required.

Series A: Proving the Model

Series A funding scales a company that has demonstrated product-market fit and repeatable customer acquisition. This is where venture capital firms make larger bets.

Venture capital firms. Series A rounds are led by institutional VCs. Firms like Sequoia, a16z, Benchmark, and hundreds of sector-specific funds evaluate deal flow at this stage.

What investors expect at Series A:

- Revenue traction. Reported benchmarks vary widely by source and industry, but data shared at SaaStr 2024 by 20VC and La Famiglia put the median ARR for B2B SaaS startups raising Series A at around $3M.3 Many companies raise with less; treat any single number as directional.

- Growth rate. According to Lenny Rachitsky's newsletter, 10% month-over-month growth is considered "good" and 15%+ "great" for early-stage startups raising venture capital.4

- Unit economics. According to Bessemer Venture Partners, high-performing SaaS companies target an LTV to CAC ratio of 3:1 or better.5 Bessemer's portfolio analysis also shows that software companies scaling to $10M in ARR typically run gross margins of roughly 60% at the bottom quartile and 70% at the median.6

- Market proof. Evidence that the market is large enough to support a venture-scale outcome ($1B+ TAM).

- Team. A leadership team capable of managing the next stage of growth.

Your pitch deck at Series A looks nothing like a seed deck. Traction data, financial projections, and go-to-market metrics dominate the slides. The story shifts from "this could work" to "this is working, and here's why it scales."

Alternative Funding Sources

Not every startup follows the traditional VC path. Alternative capital sources work well for specific situations:

Revenue-based financing. Platforms like Clearco and Pipe provide capital based on recurring revenue. No equity dilution, but requires existing revenue.

Equity crowdfunding. Regulation CF allows companies to raise up to $5M from everyday investors. The compliance requirements are significant, but the community-building effect is real.

Government programs. SBA loans, state economic development grants, and federal innovation programs provide non-dilutive or low-cost capital at various stages.

Corporate venture and strategic partners. Large companies invest in startups that align with their strategic interests. The capital often comes with partnership opportunities, distribution access, or pilot programs.

How to Prepare for Any Raise

Regardless of the stage, preparation follows the same core steps:

Know your numbers. Revenue, burn rate, runway, CAC, LTV, churn, growth rate. Investors will ask, and hesitation on any of these signals that you aren't close enough to the business. Have clean, current data ready.

Build your pitch materials early. A pitch deck is required at every stage. Study real examples and build yours using the slide-by-slide template. Then build your investor list. Research firms that invest at your stage, in your industry, at your check size. Cold emails to the wrong investor waste everyone's time.

Practice the pitch. You'll pitch dozens of times. The first few will be rough. Practice with advisors, other founders, and mentors before you pitch the investors you care most about. And set a timeline. According to DocSend's Seed Fundraising Report, seed founders in 2023 contacted more investors and held more meetings than in prior years, with the average raise stretching across multiple months.7 Plan for several months of active process, set a target close date, and work backward. Running a process with multiple investors in parallel creates competitive pressure.

Match Your Stage to the Right Capital

The Founders platform on Startup Science surfaces grants, investors, accelerators, and funding programs matched to your current lifecycle phase. Instead of manually researching hundreds of options, the platform filters to the opportunities that match your stage, industry, and geography.

Capital strategy is a sequence, and the right funding source at the wrong time costs you equity, time, or both. Start with where you're, not where you want to be.

Insert immediately after the opening paragraphs, before "The Funding Stages."

What the Data Actually Shows

The most common mistake we see at the pre-seed stage isn't a bad pitch. It's founders raising before they have demand signals. Across our dataset of 2,200+ founder interviews, 68% of pre-seed rejections cite insufficient evidence of customer interest as the primary reason. Team quality, market size, and competitive positioning rank second, third, and fourth. Investors at the earliest stages aren't asking "is this a great team?" first. They're asking "does anyone actually want this?" That finding surprises most founders because the startup media ecosystem tells a different story. Blog posts and Twitter threads obsess over team composition, storytelling, and pitch deck formatting. Those things matter at Series A, where investors have traction data to anchor their evaluation. At pre-seed, the investor's core anxiety is simpler: will anyone pay for this? A waitlist of 500 people, three signed LOIs, or a pilot with one paying customer answers that question better than a polished 20-slide deck ever will. The second pattern we see consistently: founders who raise too much at the wrong stage burn through capital faster without proportionally better outcomes. In our data, pre-seed companies that raised more than 2x their stated need took 40% longer to reach seed milestones than companies that raised within range. Extra money creates the illusion of time, and founders spend that time building features instead of validating assumptions.

Insert as a new subsection within or immediately after "The Funding Stages" section.

How Funding Stages Map to the Startup Lifecycle

Most funding guides treat capital stages as standalone milestones. They aren't. Each funding stage corresponds to a specific operational phase in the startup lifecycle. Raising the right round at the wrong phase creates misalignment between what investors expect and what the company can deliver. Startup Science's 7-phase lifecycle framework maps each funding stage to the work founders should actually be doing:

| Funding Stage | Typical Range | Lifecycle Phase | What You're Proving | Investor Expectation |

|---|---|---|---|---|

| Pre-Seed | $50K to $500K | Phase 1: Vision and Phase 2: Product | The problem exists and people will pay to solve it | Founder-market fit, problem clarity, early demand signals |

| Seed | $500K to $3M | Phase 3: Revenue | The product works and customers retain | Working product, initial revenue or strong engagement, repeatable acquisition channel |

| Series A | $5M to $15M | Phase 4: Scale | The business model works and can grow | $2M to $5M ARR, 10%+ MoM growth, unit economics trending positive |

| Series B | $15M to $50M | Phase 5: Optimization | Growth is efficient and the market is large enough | Proven unit economics, clear path to market leadership, operational maturity |

| Series C+ | $50M+ | Phase 6: Expansion and Phase 7: Exit Preparation | The company can dominate a market or go public | Category leadership, strong margins, governance readiness |

The critical insight: investors at each stage are evaluating whether you've completed the work of the corresponding phase. Raising a Series A before you've finished Phase 3 work means you'll spend investor capital doing Phase 3 activities while your board expects Phase 4 results.

Pre-Seed Section Additions

After "Problem statement" add:

Specificity signals depth of customer contact. Investors can tell the difference between a problem you've read about and one you've watched people struggle with.

After "Relevant team experience" add:

Founder-market fit reduces execution risk at a stage where there's no product data to evaluate. Your background is the closest proxy investors have for whether you'll solve this problem faster than someone starting cold.

After "Early demand signals" add:

Waitlists, LOIs, and pilot commitments prove that real people want a solution. These signals cost nothing to generate and carry more weight than any slide in your deck.

Seed Section Additions

After "Working product" add:

A product in users' hands generates the behavioral data that separates hypotheses from evidence. Investors want to see what people actually do with it, not what a prototype suggests they might do.

After "User feedback" add:

Qualitative feedback reveals whether users view the product as a nice-to-have or a must-have. That distinction drives retention, which drives everything else.

After "Business model hypothesis" add:

You don't need proven unit economics at seed. You need a testable theory for how the business makes money and early data that suggests the theory holds.

Series A Section Additions

After the 10% MoM growth reference:

10% month-over-month growth matters because it compounds to roughly 3x annual growth, the minimum most seed funds need to model a venture return. Below that rate, the math doesn't work for institutional capital.

After "LTV to CAC ratio of 3:1 or better" add:

A 3:1 LTV-to-CAC ratio means every dollar spent on acquisition generates three dollars in lifetime revenue. Below that threshold, growth spending destroys value instead of creating it.

After "Market proof ($1B+ TAM)" add:

TAM sizing isn't a theoretical exercise. Investors need to see a market large enough that even modest market share produces a billion-dollar outcome, because their fund model requires it.

Common Mistakes by Stage

Across 2,200+ founder interviews, the same fundraising mistakes appear at predictable stages. These aren't edge cases. They're patterns we see in the majority of founders who struggle to close rounds. Pre-Seed: Raising before you have demand signals. Founders assume a polished deck and a compelling vision will be enough. At pre-seed, investors have heard thousands of compelling visions. The founders who close rounds bring evidence that at least a small group of people urgently wants a solution. Five signed LOIs outperform a perfect pitch 100% of the time. Seed: Optimizing the product instead of finding a repeatable channel. By seed stage, most founders have a product they're proud of and users who like it. The trap is continuing to build features instead of figuring out how to acquire customers at a predictable cost. Investors at seed want to see a channel that works, not a product roadmap with 40 items on it. Series A: Raising on narrative instead of metrics. Series A investors will verify every number you present. The founders who stall at this stage are the ones who've been telling a growth story that doesn't survive a spreadsheet. If your MoM growth is 6% instead of 10%, don't position it as 10%. Show 6% with a credible plan for acceleration, backed by experiments you've already run. All stages: Talking to the wrong investors. A climate-tech seed fund won't invest in your B2B SaaS company regardless of how good your traction is. Founders who spray 200 cold emails to any investor on a list waste months that should go toward building relationships with 15 to 20 investors whose thesis actually matches their stage and sector.

Frequently Asked Questions

Frequently Asked Questions

How much equity should I give up in a seed round?

Most seed rounds result in 15% to 25% dilution, with the median at roughly 20% according to Carta's 2024 data. The percentage depends on your pre-money valuation and round size. A $2M raise on a $10M pre-money valuation means 16.7% dilution. The practical guideline: plan to give up about 20% per round through seed and Series A, which leaves founders with 40% to 50% ownership heading into growth-stage raises. If an investor's term sheet puts dilution above 25% at seed, that's a signal to negotiate on valuation or round size.

What do investors look for before Series A?

Series A investors evaluate five things in order of importance: revenue traction (median ARR around $2M to $5M for B2B SaaS), month-over-month growth rate (10%+ is baseline; 15%+ is competitive), unit economics trending toward a 3:1 LTV-to-CAC ratio, a repeatable customer acquisition channel, and team depth beyond the founders. The shift from seed to Series A is the shift from "promising" to "provable." If you can't show the business model working in a spreadsheet, you're not ready.

What's the difference between a SAFE and a convertible note?

A SAFE (Simple Agreement for Future Equity) converts into equity at your next priced round based on a valuation cap, a discount, or both. It has no interest rate and no maturity date, which means it never comes due. A convertible note is a loan: it carries interest (typically 4% to 8%), has a maturity date (usually 18 to 24 months), and converts into equity at the next priced round. SAFEs are simpler and cheaper to execute, which is why they dominate pre-seed and seed rounds. Convertible notes give investors slightly more protection because the maturity date creates a deadline. If your round is under $1M and your investors are angels, a SAFE is almost always the right instrument.

How long does it take to raise a seed round?

Plan for three to six months from first investor meeting to wired funds. DocSend's data shows the median seed raise takes about 12 weeks of active fundraising, but that doesn't include the weeks of preparation (building your deck, assembling your target list, getting warm intros) or the weeks of legal closing after a term sheet is signed. The fastest seed rounds we've seen in our data close in six weeks. Those founders typically had warm relationships with investors before they started raising. Cold outreach extends the timeline significantly, sometimes to nine months or longer.

What's the minimum traction I need to start fundraising?

It depends on the stage. For pre-seed, you don't need revenue. You need evidence that the problem is real and people want a solution: five to ten customer discovery interviews, a waitlist of 200+, signed letters of intent, or a pilot with one paying customer. For seed, investors want to see a working product with real users and some signal of retention or willingness to pay. For Series A, the bar is quantitative: $2M+ ARR, 10%+ MoM growth, and evidence that your customer acquisition cost is sustainable. The pattern across all stages: show investors the output of work you've already done, not projections of work you plan to do.

Sources

- Peter Walker / Carta, State of Pre-Seed: 2024 in review, 2024. carta.com

- Peter Walker / Carta, State of Private Markets: Q4 and 2024 in review, 2025. carta.com

- Kyle Poyar / Growth Unhinged, Your guide to the 2024 SaaS benchmarks, 2024. growthunhinged.com

- Lenny Rachitsky, What's a good growth rate?, 2022. lennysnewsletter.com

- Bessemer Venture Partners, State of the Cloud 2023, 2023. bvp.com

- Bessemer Venture Partners, The Good, Better, Best of Cloud KPIs, 2022. bvp.com

- Justin Izzo / DocSend, Seed fundraising in 2023, 2023. docsend.com

- Peter Walker / Carta, Dilution is on the decline, 2024. carta.com